Politics Is About To Have You And Your Portfolio 'Seeing Red' - Seeking Alpha

Mao Zedong linked politics to economics, but lately the tie between politics and markets might make him see red.

That's from a Wells Fargo note out earlier this month.

There are all kinds of fun "red" puns in there, but the salient question for investors is this: will politics make your portfolio "see red" in the year ahead?

As the Heisenberg crowd is acutely aware, my answer to that question is "yes."

Well, actually my answer is "probably." There are no certainties, a fact that seems to drive some readers to the edge of insanity.

Sorry, but I can't tell you where the S&P (NYSEARCA:SPY) is going to end up in December. Just like I can't tell you where the 10Y (NYSEARCA:TLT) is going to be six months from now.

What I can endeavor to do, however, is explore what factors will influence asset prices going forward. As I'm fond of reminding readers who insist that posts should include some kind of concrete, bullet point summary at the end, making definitive statements is pointless precisely because while we can quantify the fundamentals, we can't quantify what we might call "exogenous influence."

I know, for instance, that credit is trading rich and that the fundamentals are poor. But my contention that spreads can't compress much further is grounded just as much in the potential for exogenous factors to drive spread decompression as it is in the notion that the cycle is turning.

You get the idea.

The problem for investors in the current environment is that macro is increasingly driving markets. And macro is now almost entirely beholden to politics. That, in turn, means markets are at the mercy of geopolitical developments more so than ever before.

That of course fits nicely with what I like to call the Heisenberg raison d'être. Recall what JPMorgan's quant wizard Marko Kolanovic said earlier this month:

Various quantitative and qualitative metrics indicate that markets have become more macro driven and react faster to the new information.

And recall my response:

Between central banks and geopolitics, markets are becoming more macro driven. At the same time, it's becoming more important for average investors to understand ostensibly complex corners of the market and how they interact with the increasingly precarious macro environment. Indeed, Kolanovic has just described the Heisenberg raison d'être.

As I highlighted in "Boiling Frogs" and "Your Portfolio Needs The Status Quo," there's a general tendency for investors to extrapolate from the Brexit and Trump experiences. That's probably a mistake.

First of all, markets collapsed after the Brexit vote and US futs collapsed when it became readily apparent that Trump was going to win. Yes, those downturns were fleeting, but they happened.

Second, we've seen significant FX and rate volatility as a result of political outcomes over the past eight or nine months and eventually, that's going to spill over into equities.

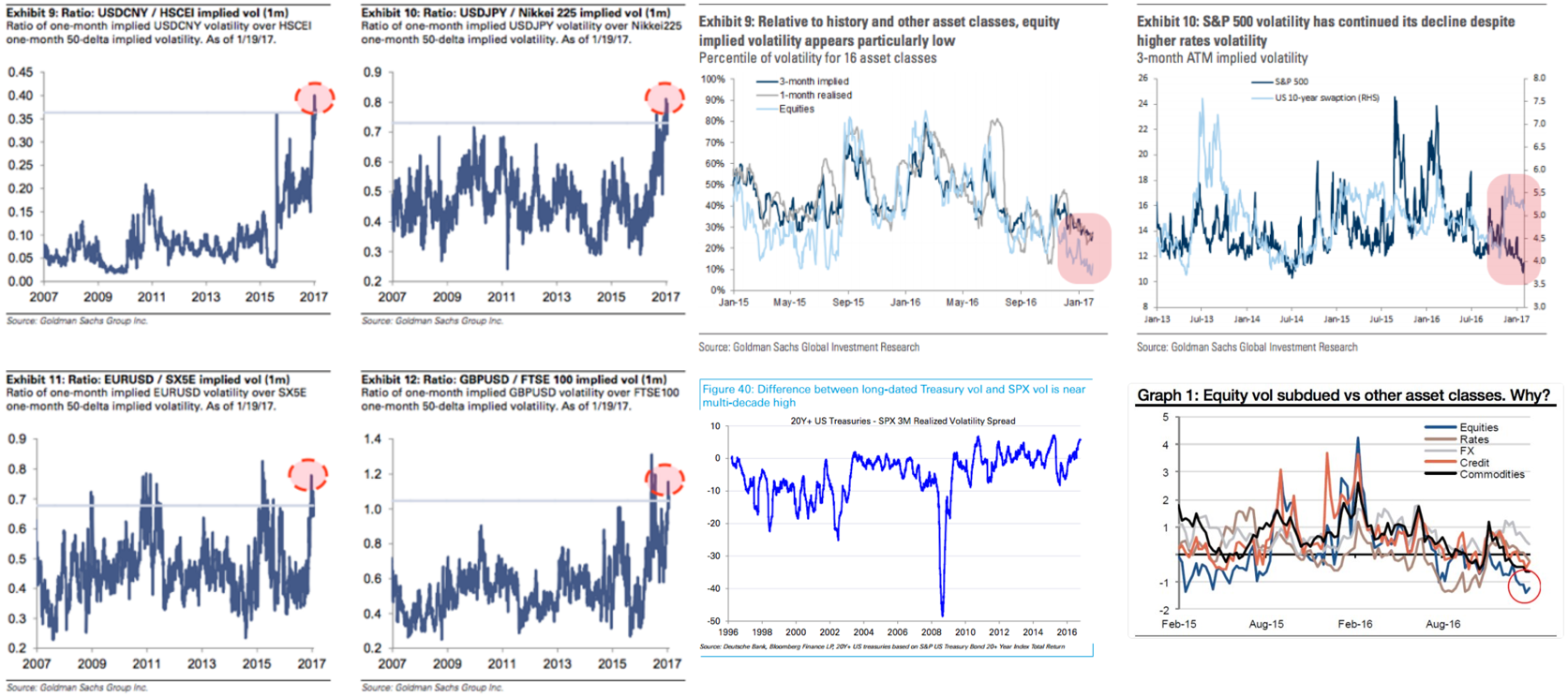

The evolution of volatility (NYSEARCA:VXX) as an asset class has led to changes in market structure that, as SocGen notes, may have antiquated headline VIX as a useful measure of market angst. Don't forget about these charts, which collectively illustrate the disconnect between rates/FX volatility and equity volatility:

(Charts: Goldman, Deutsche Bank, SocGen) Also, have a look at the following from Wells Fargo which depicts daily 10Y yield changes for three periods, one surrounding Brexit, one between Brexit and Trump, and one from Trump until now: (Chart: Wells Fargo) See why that's important? All of the outsized moves were around the big political events. Hence Wells' amusing "hysteriagram" label. Here's some color from the bank (my highlights): We plot distributions of daily changes in the 10yr Treasury yield for three periods: the past two months, i.e., dawn of the Trump era, the period immediately prior to the U.S. election, and the time around the Brexit vote. In other words, one fairly tame period is sandwiched between what we consider to be the two biggest political events of the past several years. Interestingly, the 10yr's recent moves map pretty well to its behavior around Brexit. In both cases, political uncertainty has led to market "hysteriagrams." Now needless to say, we're facing perhaps the most disruptive political event yet in the upcoming French elections. I've written extensively about this of late, noting that Marine Le Pen's promise to take France out of the EMU would likely trigger a default on something like €1.7 trillion in French public debt. "Traders remain nervous after they failed to predict the two biggest political shocks of 2016, the UK's Brexit vote and the election of Donald Trump [and while] in France, polls suggest the National Front leader Marine Le Pen will come second in the election in May, investors have been pricing in the increased risk of an FN victory," FT wrote over the weekend, adding that "the term redenomination risk has flared anew, with bond investors looking at the fine print of deals and whether euro-denominated sovereign debt could switch back into former national currencies." Right. And it's not just public debt. Consider this from Citi: While there is no explicit guidance, to our knowledge, it seems implausible that other domestic-law contracts, including corporate debt, would not be redenominated as well. We estimate that, of the €770bn of €-denominated bonds from French IG corporates, c.€300bn have been issued under French law. There has been some speculation Collective Action Clauses might offer domestic bond holders some protection. Professors Mark Weidemaier and Mitu Gulati have written in the FT that "these CACs require a super-majority of investors (in principal amount) to approve any changes to the currency of the bond". However, we think it rather unlikely that these would supersede the Lex Monetae, which allows a sovereign to choose its currency. Oh, and don't forget about the Netherlands, where Geert Wilders (who once advocated locking male asylum seekers up to keep "Islamic testosterone bombs" away from European women - and yes, that's real) insists that the "populist genie is out of the bottle." Here are a few quick excerpts from a recent article in The Telegraph: The populist revolution sweeping Europe will continue even if candidates like Marine Le Pen and Austrian far-Right parties do not win power in coming elections, Geert Wilders, the leading Dutch anti-immigrant fireband, predicted on Wednesday. Currently topping the polls ahead of next month's parliamentary elections in the Netherlands, Mr Wilders said that the European Union's failure to grasp popular anger meant that the nationalist "genie" could never be put back in the bottle in Europe. Again, this isn't meant as a partisan statement. It's simply designed to show you that this is real and it has real implications for asset prices. More to the point, even if you don't own the assets it affects, you will invariably feel the reverberations. Think about how erratically markets traded around the Greek bailout negotiations and around the Chinese yuan devaluation. And yes, think about how markets moved around Brexit and Trump. Now picture what would happen if a candidate who has threatened a €1.7 trillion sovereign default were elected. Remember, these candidates don't have to win to jar the market. "We think the focus on polls is likely to continue from here but, given the precedents, we expect market reaction to be skewed towards pricing higher risk premia than otherwise," BofAML wrote on Friday, adding that "while it appears unlikely that a Dutch government could take the country out of the EU post-elections, the market may become increasingly nervous if polls end up underestimating voters' preference for populist parties." And wouldn't you know it, there's quite a bit of entanglement going on here. Look, for instance, at Dutch banks' claims on France as a percentage of total assets versus the same measure for other EU banking systems: (Chart: BofAML) Of course, Dutch spreads have, like OAT spreads, widened versus German bunds although Dutch CDS hasn't blown out commensurately (so you know, if you're in the market for sovereign CDS exposure, there's your play):

No comments :